国际经济管理学院研究生workshop 2024年春季学期第2期(第一组)

时间: 2024-03-25 04:10:00

研究生workshop由首都经济贸易大学国际经济管理学院主办。主要内容:一是研究生报告前沿或经典文献,二是研究生报告自己的研究或研究设想。论坛宗旨是:为学院师生搭建一个学术交流平台,营造浓厚学术氛围;通过对经典论著或前沿文献的研讨,拓宽研究生的理论视野,提升研究生的前沿方法运用能力,帮助研究生提高论文写作质量。

本期workshop

报告人:郑雅璇(博士二年级)

导师:李鲲鹏

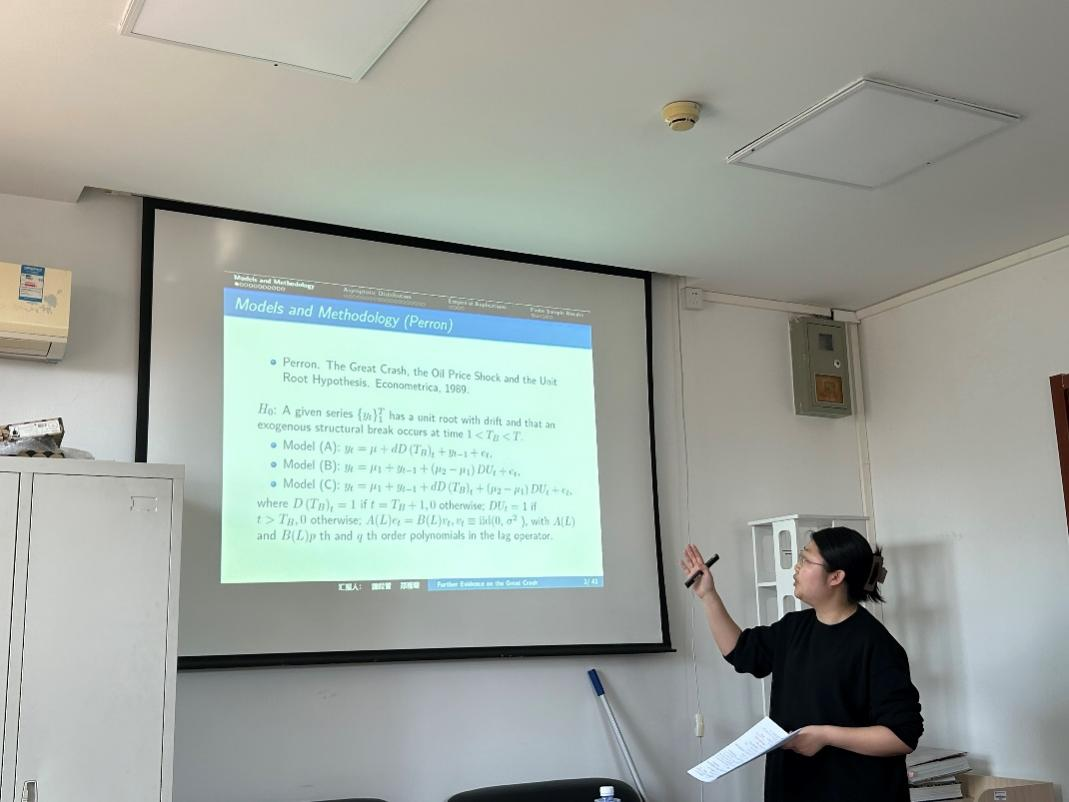

报告题目:《Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis》, Journal of Business & Economic Statistics, 1992.

报告摘要:

Recently, Perron has carried out tests of the unit-root hypothesis against the alternative hypothesis of trend stationarity with a break in the trend occurring at the Great Crash of 1929 or at the 1973 oil-price shock. His analysis covers the Nelson-Plosser macroeconomic data series as well as a postwar quarterly real gross national product (GNP) series. His tests reject the unit-root null hypothesis for most of the series. This article takes issue with the assumption used by Perron that the Great Crash and the oil-price shock can be treated as exogenous events. A variation of Perron's test is considered in which the breakpoint is estimated rather than fixed. We argue that this test is more appropriate than Perron's because it circumvents the problem of data-mining. The asymptotic distribution of the estimated breakpoint test statistic is determined. The data series considered by Perron are reanalyzed using this test statistic. The empirical results make use of the asymptotics developed for the test statistic as well as extensive finite-sample corrections obtained by simulation. The effect on the empirical results of fat-tailed and temporally dependent innovations is investigated. In brief, by treating the breakpoint as endogenous, we find that there is less evidence against the unit-root hypothesis than Perron finds for many of the data series but stronger evidence against it for several of the series, including the Nelson-Plosser industrial-production, nominal-GNP, and real-GNP series.

报告人:梁华宇(博士二年级)

导师:李鲲鹏

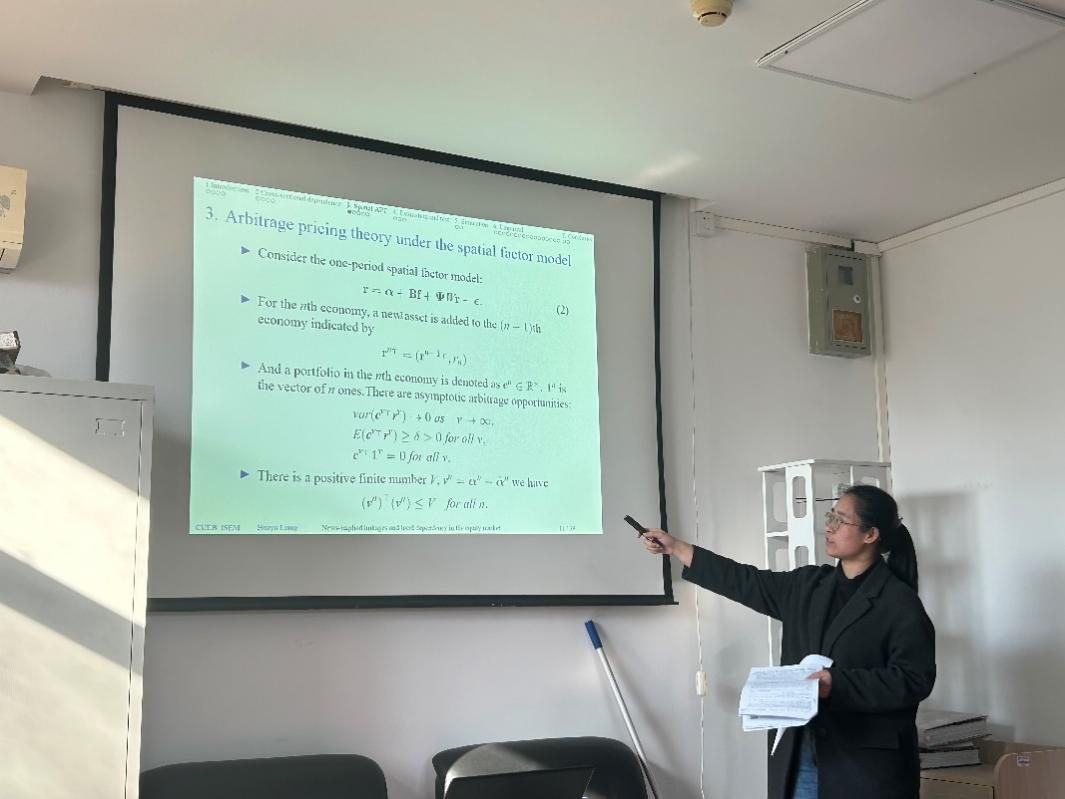

报告题目:《News-implied linkages and local dependency in the equity market》, Journal of Econometrics, 2023.

报告摘要:

This paper studies a heterogeneous coefficient spatial factor model that separately addresses both common factor risks (strong cross-sectional dependence) and local dependency (weak cross-sectional dependence) in equity returns. From the asset pricing perspective, we derive the theoretical implications of no asymptotic arbitrage for the heterogeneous spatial factor model, generalizing the work of Kou et al. (2018). We also provide the associated Wald tests for the APT restrictions in the general case when there are both traded and non-traded factors. On the empirical side, it is challenging to measure granular firm-to-firm connectivity for a high-dimensional panel of equity returns. We use extensive business news to construct firms’ links through which local shocks transmit, and we use those news-implied linkages as a proxy for the connectivity among firms. Empirically, we document a considerable degree of local dependency among S&P500 stocks, and the spatial component does a great job in capturing the remaining correlations in the de-factored returns. We find that adding spatial interaction terms to factor models reduces mispricing and boosts model fitting. By comparing the performance of the model estimated using different networks, we show that the news-implied linkages provide a comprehensive and integrated proxy for firm-to-firm connectivity.