国际经济管理学院研究生workshop 2023年秋季学期第4期

时间: 2023-10-17 03:02:00

研究生workshop由首都经济贸易大学国际经济管理学院主办。主要内容:一是研究生报告前沿或经典文献,二是研究生报告自己的研究或研究设想。论坛宗旨是:为学院师生搭建一个学术交流平台,营造浓厚学术氛围;通过对经典论著或前沿文献的研讨,拓宽研究生的理论视野,提升研究生的前沿方法运用能力,帮助研究生提高论文写作质量。

本期workshop

报告人:郑雅璇(博士二年级)

导师:李鲲鹏

报告题目:《Structural Changes, Common Stochastic Trends, and Unit Roots in Panel Data》,Review of Economic Studies,2009

报告摘要:

This paper studies the problem of unit root testing in the presence of multiple structural changes and common dynamic factors. Structural breaks represent infrequent regime shifts, while dynamic factors capture common shocks underlying the comovement of economic time series. We examine the modified Sargan–Bhargava (MSB) test in the panel data setting and propose ways to handle multiple structural changes and dynamic factors. Properties of the MSB test under these non-standard conditions are derived. For example, the test statistics are shown to be invariant, in the limit, to mean breaks. This invariance does not carry over to breaks in linear trends, where the test statistics will converge to functionals of weighted Brownian bridges. A simplified test statistic is then proposed, which is invariant to both mean and trend breaks. We further study pooled test statistic based on standardization and combination of p-values. Response surfaces for p-values of all test statistics are computed to facilitate the empirical implementation of the proposed methodology. The pooled tests are shown to have good finite sample performance.

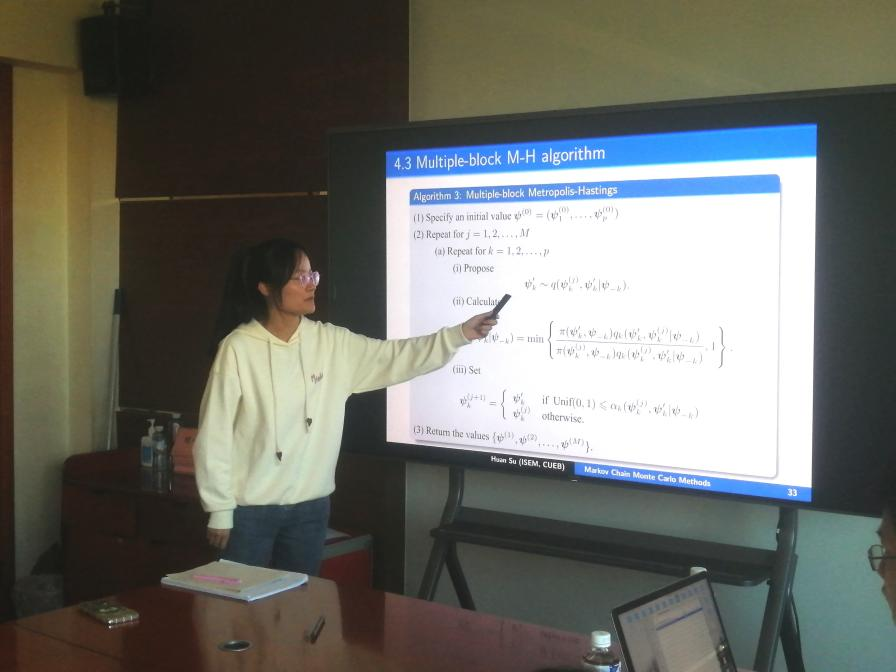

报告人:苏欢(博士一年级)

导师:李鲲鹏

报告题目:《MARKOV CHAIN MONTE CARLO METHODS: COMPUTATION AND INFERENCE》Handbook of Econometrics,2001.

报告摘要:

This chapter reviews the recent developments in Markov chain Monte Carlo simulation methods. These methods, which are concerned with the simulation of high dimensional probability distributions, have gained enormous prominence and revolutionized Bayesian statistics. The chapter provides background on the relevant Markov chain theory and provides detailed information on the theory and practice of Markov chain sampling based on the Metropolis-Hastings and Gibbs sampling algorithms. Convergence diagnostics and strategies for implementation are also discussed. A number of examples drawn from Bayesian statistics are used to illustrate the ideas. The chapter also covers in detail the application of MCMC methods to the problems of prediction and model choice.

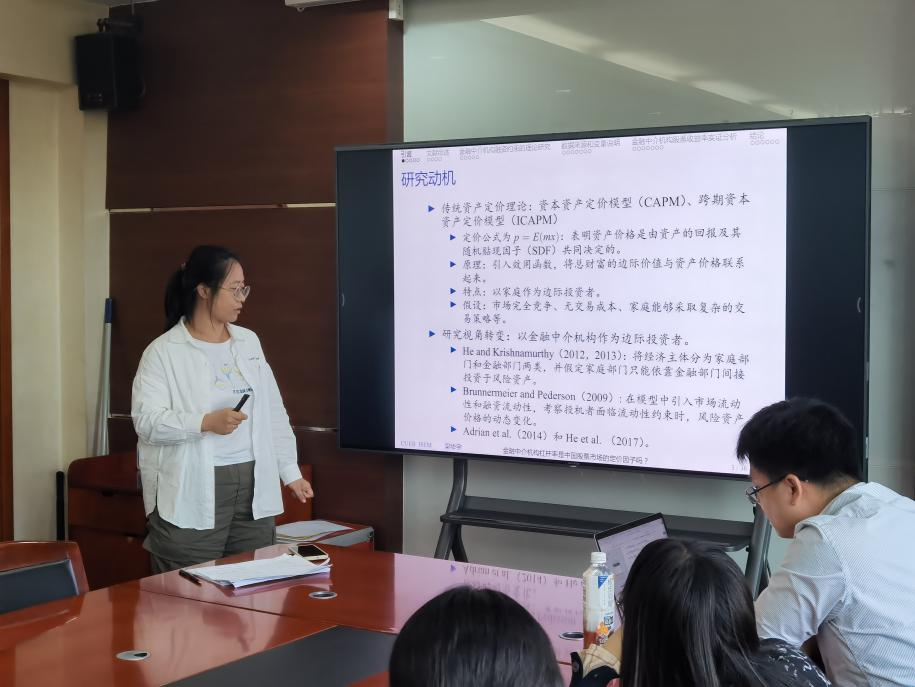

报告人:梁华宇(博士二年级)

导师:李鲲鹏

报告题目:《金融中介机构杠杆率是中国股票市场的定价因子吗? 》

报告摘要:

为了探究中国金融中介机构作为边际投资者在资产定价中的作用,本文首先梳理了金融中介机构权益融资和债务融资约束理论,表明金融中介机构杠杆率可以作为其财富边际价值的代理变量;然后,构建金融中介杠杆率因子以测度金融中介机构随机贴现因子;最后采用 Fama-MacBeth 方法研究了银行和证券公司两类金融中介机构对中国股票收益率的定价效力,之后与 Fama-French 三因子、五因子以及中国版三因子模型比较,并进行了稳健性检验。研究发现,银行杠杆率因子的风险溢价显著为负,且具有反周期性;而证券公司杠杆率因子的风险溢价并不显著。同时,比较模型之间定价误差的结果表明,杠杆率单因子模型的定价误差小于多因子模型的定价误差,但模型的 R^2 并未达到最高。稳健性检验结果表明,完整的样本区间能更好支持杠杆率因子风险溢价的解释。本文也为健全资本市场功能,充分压实中介机构责任,进一步完善我国投资者结构,培育合格机构投资者的策略提供可能的实证依据和借鉴意义。