国际经济管理学院研究生workshop 2023年秋季学期第12期

时间: 2024-01-03 03:36:00

研究生workshop由首都经济贸易大学国际经济管理学院主办。主要内容:一是研究生报告前沿或经典文献,二是研究生报告自己的研究或研究设想。论坛宗旨是:为学院师生搭建一个学术交流平台,营造浓厚学术氛围;通过对经典论著或前沿文献的研讨,拓宽研究生的理论视野,提升研究生的前沿方法运用能力,帮助研究生提高论文写作质量。

本期workshop

报告人:梁华宇(博士二年级)

导师:李鲲鹏

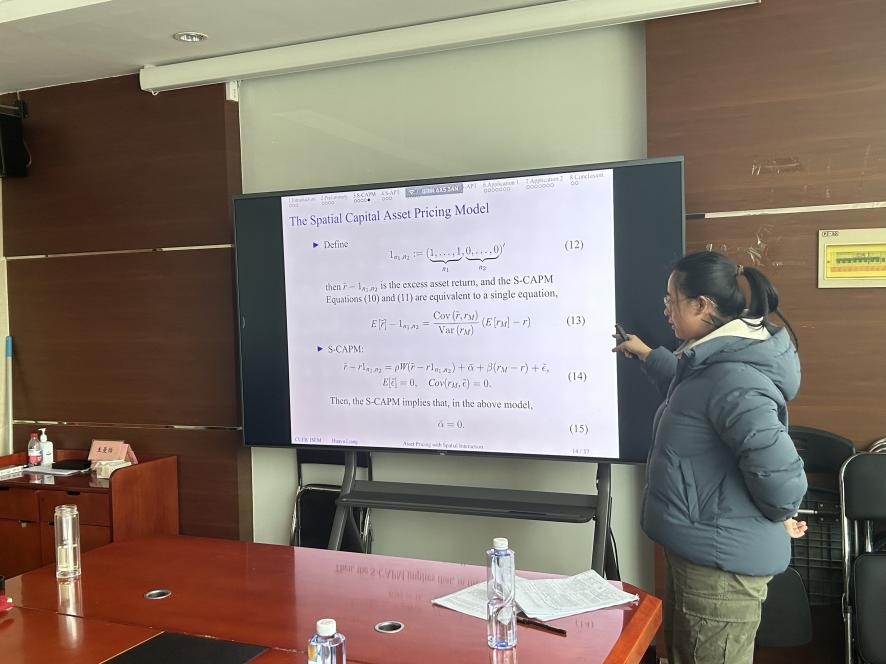

报告题目:《Asset Pricing with Spatial Interaction》,Management Science,2017.

报告摘要:

We propose a spatial capital asset pricing model and a spatial arbitrage pricing theory (S-APT) that extend the classical asset pricing models by incorporating spatial interaction. We then apply the S-APT to study the comovements of eurozone stock indices (by extending the Fama–French factor model to regional stock indices) and the futures contracts on S&P/Case–Shiller Home Price Indices; in both cases, spatial interaction is significant and plays an important role in explaining cross-sectional correlation.

我们提出了一种空间资本资产定价模型和空间套利定价理论(S-APT),通过纳入空间交互来扩展经典资产定价模型。然后,我们应用S-APT来研究欧元区股票指数(通过将Fama-French因子模型扩展到地区股票指数)和标准普尔/Case-Shiller房价指数期货合约的共同波动;在这两种情况下,空间交互都是显著的,并在解释横截面相关性方面发挥重要作用。

报告人:郑雅璇(博士二年级)

导师:李鲲鹏

报告题目:《Recursive and Sequential Tests of the Unit-Root and Trend-Break Hypotheses: Theory and International Evidence》, Journal of Business and Economic Statistics, 1992.

报告摘要:

This article investigates the possibility, raised by Perron and by Rappoport and Reichlin, that aggregate economic time series can be characterized as being stationary around broken trend lines. Unlike those authors, we treat the break date as unknown a priori. Asymptotic distributions are developed for recursive, rolling, and sequential tests for unit roots and/or changing coefficients in time series regressions. The recursive and rolling tests are based on changing subsamples of the data. The sequential statistics are computed using the full data set and a sequence of regressors indexed by a "break" date. When applied to data on real postwar output from seven Organization for Economic Cooperation and Development countries, these techniques fail to reject the unit-root hypothesis for five countries (including the United States) but suggest stationarity around a shifted trend for Japan.

这篇文章研究了由Perron和Rappoport与Reichlin提出的可能性,即总体经济时间序列可以被描述为围绕中断的趋势线是平稳的。与这些作者不同的是,我们将中断日期视为先验未知。对于单位根和/或时间序列回归中的变化系数,我们开发了递归、滚动和顺序检验的渐近分布。递归和滚动测试基于数据的变化子样本。顺序统计是使用完整数据集和一个由“中断”日期索引的回归器序列来计算的。当应用于来自七个经济合作与发展组织成员国的实际战后产出数据时,这些技术未能拒绝五个国家(包括美国)的单位根假设,但暗示着日本围绕移动的趋势是稳定的。