国际经济管理学院研究生workshop2023年春季学期第4期

时间: 2023-03-17 12:00:00

研究生workshop由首都经济贸易大学国际经济管理学院主办。主要内容:一是研究生报告前沿或经典文献,二是研究生报告自己的研究或研究设想。论坛宗旨是:为学院师生搭建一个学术交流平台,营造浓厚学术氛围;通过对经典论著或前沿文献的研讨,拓宽研究生的理论视野,提升研究生的前沿方法运用能力,帮助研究生提高论文写作质量。

本期workshop

报告人:梁华宇(2022级博士研究生)

导师:李鲲鹏

报告论文:《Heterogeneous intermediary asset pricing》Journal of Financial Economics,2021 作者:Mahyar Kargar

《异质中介资产定价》

报告摘要:

I show that the composition of the financial sector has important asset pricing implications beyond the health of the aggregate financial sector. To assess the impact of massive balance sheet adjustments within the intermediary sector during the Great Recession and resolve conflicting asset pricing evidence, I propose a dynamic asset pricing model with heterogeneous intermediaries facing financial frictions. Asset flows between intermediaries are quantitatively important for both the level of and variation in the risk premium. An empirical measure of the composition of the intermediary sector negatively forecasts future excess returns and is priced in the cross-section with a positive price of risk.

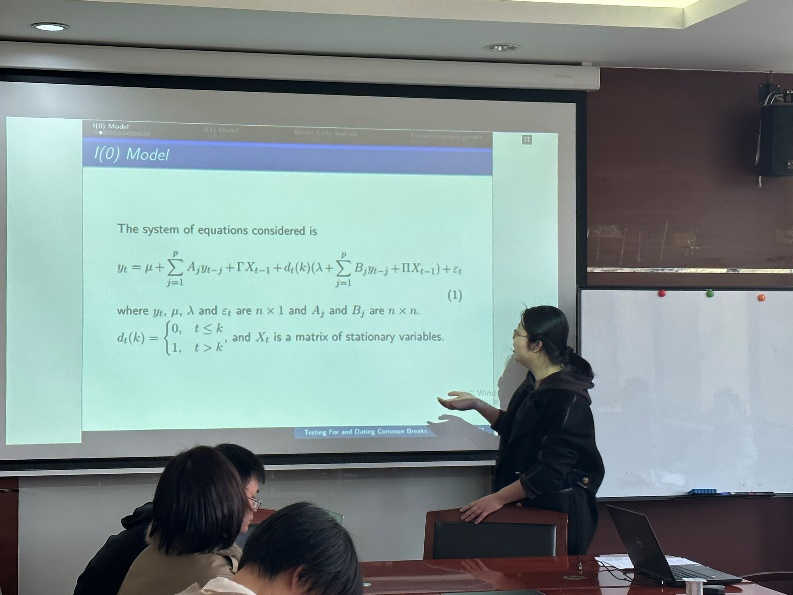

报告人:郑雅璇(2022级博士研究生)

导师:李鲲鹏

报告论文:《Testing For and Dating Common Breaks in Multivariate Time Series》 Review of Economic Studies, 1998

作者:Jushan Bai, Robin L. Lumsdaine and James H. Stock

《多元时间序列中常见断裂的检验与定年》

报告摘要:This paper develops methods for constructing asymptotically valid confidence intervals for the date of a single break in multivariate time series, including I(0), I(1), and deterministically trending regressors. Although the width of the asymptotic confidence interval does not decrease as the sample size increases, it is inversely related to the number of series which have a common break date, so there are substantial gains to multivariate inference about break dates. These methods are applied to two empirical examples: the mean growth rate of output in three European countries, and the mean growth rate of U.S. consumption, investment, and output.