国际经济管理学院研究生workshop2023年春季学期第7期

时间: 2023-04-10 02:04:00

研究生workshop由首都经济贸易大学国际经济管理学院主办。主要内容:一是研究生报告前沿或经典文献,二是研究生报告自己的研究或研究设想。论坛宗旨是:为学院师生搭建一个学术交流平台,营造浓厚学术氛围;通过对经典论著或前沿文献的研讨,拓宽研究生的理论视野,提升研究生的前沿方法运用能力,帮助研究生提高论文写作质量。

本期workshop

报告人:苏欢(2020级硕士研究生)

导师:李鲲鹏

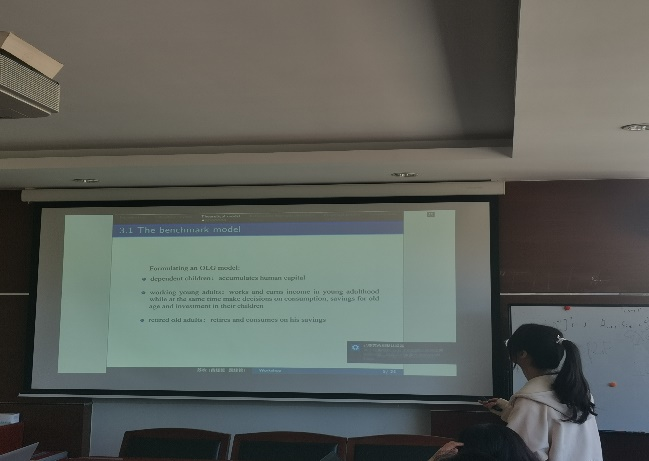

报告论文:《Intergenerational transfer of human capital and its impact on income mobility: Evidence from China》China Economic Review, 2016

作者:Xuezheng QIN, Tianyu WANG, Castiel Chen ZHUANG《人力资本代际转移及其对收入流动的影响——来自中国的经验证据》

报告摘要:

This paper analyzes theoretically and empirically the impact of intergenerational transmission of human capital on the income mobility in China. We use a three-period overlapping-generations (OLG) model to show that the human capital transfer plays a remarkable role in determining the parent-to-offspring investment in human capital and the intergenerational elasticity of income. We then estimate a simultaneous equations model (SEM) using the 1989–2009 China Health and Nutrition Survey (CHNS) data to verify our theoretical predictions. The results show that (i) human capital, measured by health and education, is directly transmitted from one generation to the next, reflecting the parent-induced inequality of development opportunities among offspring in China; (ii) the estimated intergenerational income elasticity increases from 0.429 to 0.481 when the direct transfer of human capital is accounted for, suggesting that omitting this mechanism would overestimate China's income mobility. Our findings provide policy implications on strengthening human capital investments among the disadvantaged groups, reinforcing reforms that promote equality of opportunity, and improving the efficiency of labor markets in China.

报告人:王璞(2020级博士研究生)

导师:李鲲鹏

报告论文:《Comparing cross-section and time-series factor models》The Review of Financial Studies, 2020

作者:Eugene F. Fama and Kenneth R. French《横截面因子模型与时间序列因子模型的比较》

报告摘要:

We use the cross-section regression approach of Fama and MacBeth (1973) to construct cross-section factors corresponding to the time-series factors of Fama and French (2015). Time-series models that use only cross-section factors provide better descriptions of average returns than time-series models that use time-series factors. This is true when we impose constant factor loadings