国际经济管理学院研究生workshop 2023年春季学期第14期

时间: 2023-06-19 11:59:00

研究生workshop由首都经济贸易大学国际经济管理学院主办。主要内容:一是研究生报告前沿或经典文献,二是研究生报告自己的研究或研究设想。论坛宗旨是:为学院师生搭建一个学术交流平台,营造浓厚学术氛围;通过对经典论著或前沿文献的研讨,拓宽研究生的理论视野,提升研究生的前沿方法运用能力,帮助研究生提高论文写作质量。

本期workshop

报告人:郑雅璇(2022级博士研究生)

导师:李鲲鹏

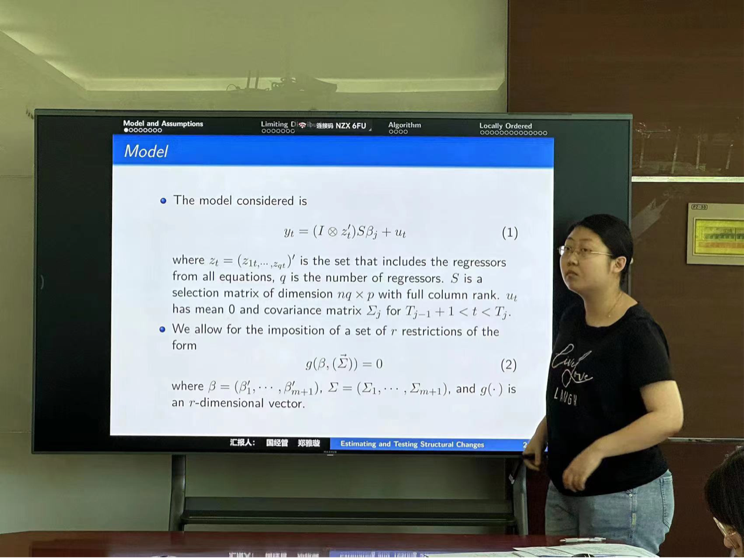

报告论文:《Estimating and testing structural changes in multivariate regressions》Econometrica, 2007 作者:Zhongjun Qu and Pierre Perron

报告摘要:

This paper considers issues related to estimation, inference, and computation with multiple structural changes that occur at unknown dates in a system of equations. Changes can occur in the regression coeffcients and/or the covariance matrix of the errors. We also allow arbitrary restrictions on these parameters, which permits the analysis of partial structural change models, common breaks that occur in all equations, breaks that occur in a subset of equations, and so forth. The method of estimation is quasi-maximum likelihood based on Normal errors. The limiting distributions are obtained under more general assumptions than previous studies. For testing, we propose likelihood ratio type statistics to test the null hypothesis of no structural change and to select the number of changes. Structural change tests with restrictions on the parameters can be constructed to achieve higher power when prior information is present. For computation, an algorithm for an efficient procedure is proposed to construct the estimates and test statistics. We also introduce a novel locally ordered breaks model, which allows the breaks in different equations to be related yet not occurring at the same dates.

报告人:梁华宇(2022级博士研究生)

导师:李鲲鹏

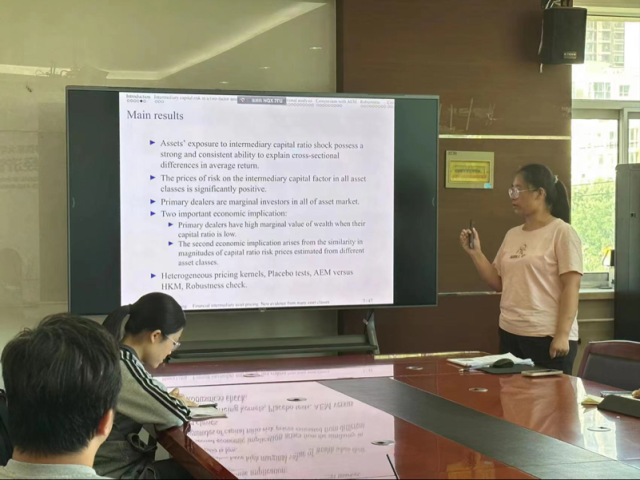

报告论文:《Intermediary asset pricing: New evidence from many asset classes》Journal of Financial Economics (2017)

作者:Zhiguo He, Bryan Kelly, Asaf Manela

报告摘要:

We find that shocks to the equity capital ratio of financial intermediaries—Primary Dealer counterparties of the New York Federal Reserve—possess significant explanatory power for cross-sectional variation in expected returns. This is true not only for commonly studied equity and government bond market portfolios, but also for other more sophisticated asset classes such as corporate and sovereign bonds, derivatives, commodities, and currencies. Our intermediary capital risk factor is strongly procyclical, implying countercyclical intermediary leverage. The price of risk for intermediary capital shocks is consistently positive and of similar magnitude when estimated separately for individual asset classes, suggesting that financial intermediaries are marginal investors in many markets and hence key to understanding asset prices.